Sunshine in Japan?

By Dr. Scott B. MacDonald

Japan's economy has long faced dark and overcast weather, with some analysts claiming it has been in an extended coma. Over the past 20 years or so, the economic situation has been defined by slow growth, a substantial build-up in govermnent debt and a difficult-to-exit deflation. Successive governments attempted to pull Japan out of its economic malaise, but generally failed. The Liberal Democratic Party (LDP) government of Prime Minister Shinzo Abe is embarking on a new effort, helped by a massive stimulus package coordinated with its central bank. While the Abe plan, also referred to s "Abenomics," carries considerable risk, it is a bold and badly-needed new direction, which has the potential to end deflation and pull Japan out of its economic cul-de-sac.

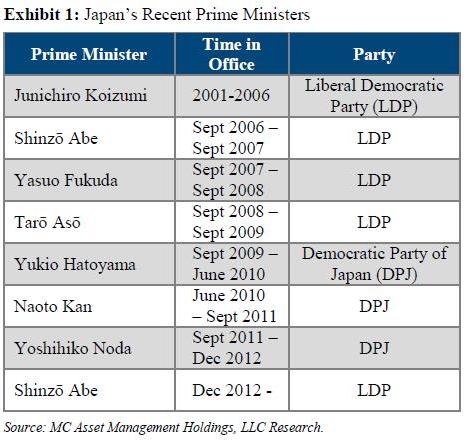

Abe's second term as prime minister is ushering in some considerable changes for Japan. Abe briefly served as the nation's leader from September 2006 to September 2007, following the highly charismatic and reform-minded Junichiro Koizumi. Abe, however, lasted only for a short time, to be followed by a rapid succession of other prime ministers (see table). This did little to generate confidence in Japan and complicated the economic decision-making process.

Abe's second time in office is radically different from the first. His party, the LDP, was keen to return to office and lined up to support their leader. The LDP had an overwhelming victory, giving Abe a mandate to take a more aggressive stance on reviving the Japanese economy. Part of that more aggressive stance was to put his ally, Haruhiko Kuroda, into the Bank of Japan's governor seat. Abe brought relentless pressure on the then conservative governor, Masaaki Shirakawa, who resigned weeks early.

On April 4th, Kuroda announced that the Japanese central bank would seek to double the country's monetary base over two years. Along these lines, the Bank of Japan has indicated it will aggressively buy longer-term bonds and double its holdings of government bonds in two years, doubling the amount of money in circulation in the process. The target is to push up Japanese inflation to 2% "at the earliest possible time." Kuroda's policies, following the quantitative mode of the Fed, are a radical turn in what some have said have been a series of halfhearted campaigns to end deflation, with its related debilitating decline in wages, prices and profits.

The core elements of Kuroda's new direction are:

- The central bank will lengthen the average maturity of its holdings of government bonds to seven years from three years.

- It will expand Japan's monetary base to ¥270 trillion ($2.8 trillion) by March 2015. Under that plan, the bank will buy ¥7 trillion of bonds each month, equal to more than 1% of its GDP. This is almost twice the pace of such purchases by the U.S. Federal Reserve.

- The Bank of Japan will also consolidate all of its purchases in a single operation in an effort to enhance transparency of the bank's purchases.

Bond and equity markets have responded favorably to Kuroda's new central bank policies. One beneficiary of the Bank of Japan's buying spree is Europe. Merrion Economics' Alan McQuaid observed: "European bond markets now seem to think there is a new, unconditional buyer in town, namely Japan. The scenario is that a weakened yen will lead Japanese investors to load up on foreign assets. Even if they stick to high quality, or so called 'core' bonds, that could trickle down to 'peripheral' debt as well." We have already seen some degree of spread compression with European five-year sovereign CDS since the April 4th announcement. Whether the expected Japanese wall of money arrives in Europe is yet to be confirmed by data. That said, the psychological effect has been positive.

The ultimate success of the new direction remains an open debate. Indeed, some economists are concerned that the Bank of Japan's large acquisitions of government debt could eventually be looked upon by investors as facilitating runaway public spending. In turn, such a view could undermine confidence in the government's ability to bring its massive public sector debt under control or to raise long-term interest rates. Still other economists worry that, once inflation starts to rise, it will be difficult to control.

Our view is that Abe and Kuroda are on the right track - for now. Markets have responded with confidence, foreign investors are looking again at Japan, and the yen has depreciated from the 80s to around 100 to the U.S. dollar. Yen devaluation is critical to help restimulate the export sector that was hurt by a strong yen (it became a safe harbor currency following Europe's sovereign debt crisis). At the same time, monetary policy alone cannot end deflation. In the U.S., the Fed's quantitative easing has probably helped keep the economy moving, but the U.S. Congress and the Presidency have been negligent until recently in conducting economic policy. It is the same issue in Japan - to really change direction, the Diet and Prime Minister also have to do their parts. This means the government must also tackle difficult problems related to a shrinking and aging population and layers of regulations that maintain inefficiencies in daily economic life. Along these lines, we fully concur with Bloomberg's William Pesek: "Prime Minister Shinzo Abe must match BOJ action with equally aggressive structural changes and pro-growth strategies to generate true confidence on the part of households, companies and investors." No doubt U.S. economic growth would be on sounder footing if the President and Congress agreed on policies and implemented them.

Is it time for some sunshine in Japan? We would argue that, although many clouds remain, there are patches of sunlight. The real measures of success will be watching inflation and economic growth data, followed by better corporate results and eventually hiring and wage increases. We are still waiting for sunshine in Japan, but there is growing confidence that the sunscreen cream put away long ago will be useful as 2013 progresses.

"This article originally appeared in The Global Economic Reporter, published by MC Asset Management Holdings, LLC, a subsiduary of Mitsubishi Corporation"

While the information and opinions contained within have been compiled from sources believed to be reliable, KWR does not represent that it is accurate or complete and it should be relied on as such. Accordingly, nothing in this article shall be construed as offering a guarantee of the accuracy or completeness of the information contained herein, or as an offer or solicitation with respect to the purchase or sale of any security. All opinions and estimates are subject to change without notice. KWR staff, consultants and contributors to the KWR International Advisor may at any time have a long or short position in any security or option mentioned.

KWR International Advisor

Editor: Dr. Scott B. MacDonald, Sr. Consultant

Deputy Editors: Dr. Jonathan Lemco, Director and Sr. Consultant and Robert Windorf, Senior Consultant

Publisher: Keith W. Rabin, President

To obtain your free subscription to the KWR International Advisor,

please click here to register for the KWR Advisor mailing list

For information concerning advertising, please contact:

Advertising@kwrintl.com

Please forward all feedback, comments and submission and reproduction requests to:

KWR.Advisor@kwrintl.com

Website content © KWR International